Realtors defend homebuyers over Biden's 'unnecessary' mortgage rule: 'Not the time for fee increases'

'Given the sharp increase in mortgage rates over the last year, no homebuyers should face higher fees,' the NAR said in a letter to the FHFA

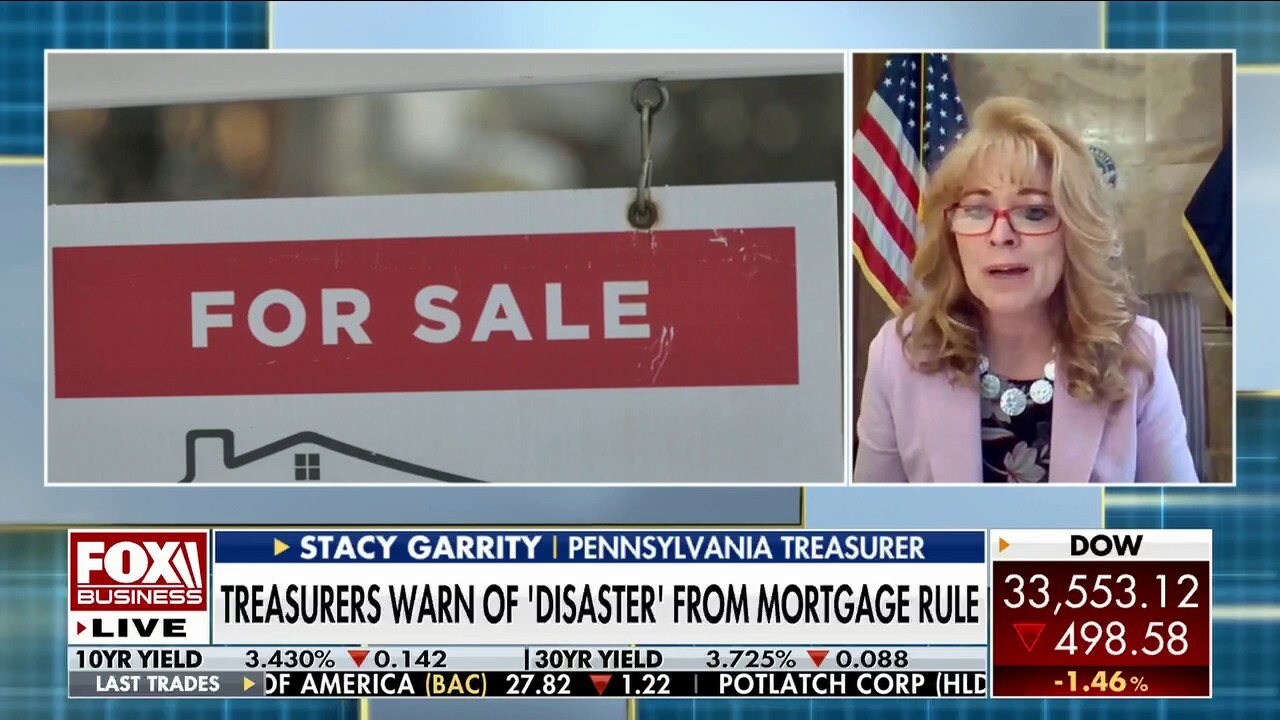

PA Treasurer Stacy Garrity blasts Biden's new mortgage rule punishing borrowers with good credit: 'Disaster'

Pennsylvania Treasurer Stacy Garrity provides insight into President Biden's new mortgage rule to subsidize risky loans.

America’s largest trade association is sticking up for homebuyers after the Biden administration enacted new rules that will force borrowers with good credit to subsidize risky mortgages.

In a letter obtained by Fox News Digital to the Federal Housing Finance Agency (FHFA), Kenny Parcell, the 2023 president of the National Association of Realtors (NAR), expressed concern over the fees which went into effect on May 1, arguing changes are "unnecessary" and "should be eliminated."

"Given the sharp increase in mortgage rates over the last year, no homebuyers should face higher fees," it read.

The NAR has more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

"Realtors are hearing from their clients concerned about fee increases and are helping them navigate the process," a NAR spokesperson told Fox News Digital. "It is important buyers receive accurate information about these fees, especially with so many incomplete narratives circulating that fuel unnecessary anxiety. Lenders have been factoring these unfortunate fee increases for months, so most buyers under contract have already locked in rates with the fees. And those looking to buy have been qualified based on the higher rates."

Biden’s plan outlined just a few weeks ago by the FHFA aims to help lower-income borrowers afford their monthly mortgage payment. Under it, borrowers with a credit score of 679 or lower and less money for a down payment will qualify for better mortgage rates than they otherwise would have, while those with higher ratings ranging from 680 to above 780 will pay increased fees.

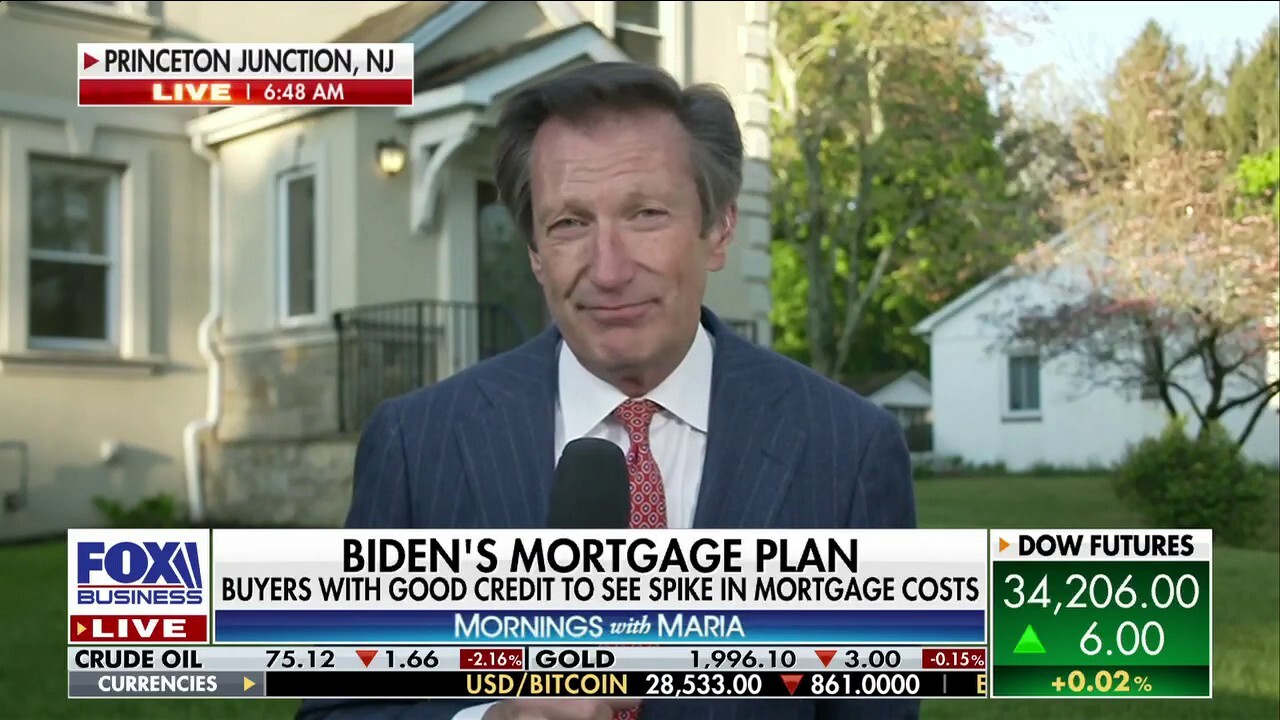

Healthy credit home buyers now have to 'pay for other people's mortgages': David Stevens

FOX Business' Jeff Flock reports from Princeton Junction, New Jersey, where President Biden's mortgage redistribution plan takes effect Monday.

A person's credit score is one of the most important indicators of creditworthiness for lenders, helping to determine if a prospective borrower will qualify for a loan and what interest rate will apply.

New York licensed real estate salesperson-certified buyer representative (CBR) Brittany Sandarciero told Fox News Digital the new rules are "disheartening" and do not get to the "root of the problem."

"It's disheartening because a lot of Americans struggle to save for a house and down payment," she said. "There's people that sacrifice and save for a rainy day… Even though [the FHFA] are doing their best to make homeownership affordable for everyone, there's a better way to go about it."

FORMER OBAMA HOUSING CHIEF SLAMS BIDEN'S ‘UNPRECEDENTED’ MORTGAGE PLAN: ‘NOT THE WAY TO DO IT’

Manhattan broker Brian Lewis, a.k.a. "America's Agent," also shared his frustrations over the changes on "Mornings with Maria" Monday.

"I think that putting people in a position to take a place that they really can't make happen is a recipe for disaster," he said.

"Does my industry need one more boot on our neck to hold us down? Interest rates have gone up, we're just getting our stride, and now this," Lewis continued.

President Biden is facing backlash for his administrations changes to mortgage rates for low credit homebuyers. (AP Photo/Evan Vucci / AP Newsroom)

One of the significant changes comes to loan level pricing adjustments (LLPAs). The structure was introduced around the 2008 housing crisis and offered a way for government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac to adjust loans for riskier buyers. They remain in effect today.

The NAR calculated that a borrower with a 730-credit score and 17% down payment could see their annual mortgage rate "jump" by 6 to 6.15%.

"It's another deterrent that's come for everyone because the interest rates were affordable," Sandarciero said. "And now the interest rates are high, and house prices are high, and it's just going to make real estate more unaffordable."

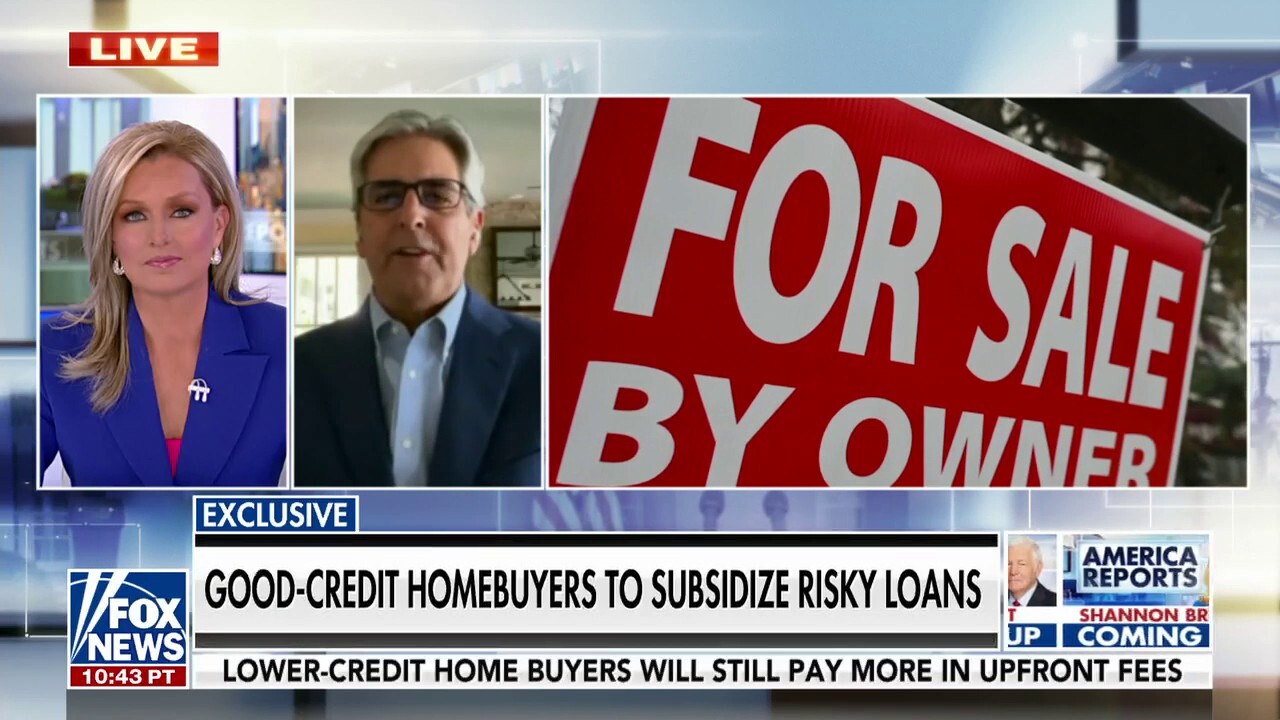

Former Obama housing chief slams ‘unprecedented’ Biden mortgage plan

Former Obama Federal Housing Association Commissioner David Stevens warns against the White House redistributing high-risk loan costs to homeowners with good credit.

Lewis argued that the fee changes are also simply unfair to American homeowners and homebuyers.

"I do think that some of these people who will benefit from this program are not necessarily people who will not pay their loans back. But nobody paid for my ticket. I worked for it, and I worked my way up. And I think that's the way to do it," America’s Agent explained. "And I don't think it's to penalize the people who are already facing higher interest rates."

The NAR noted it appreciated "this important change given the spike in mortgage rates and strong price growth in recent years that weigh on affordability for all homebuyers," but cautioned it is an "unnecessary" fee hike.

BIDEN'S SOCIALIST MORTGAGE PLAN IS STUDENT LOAN HANDOUTS 2.0

"The fee increase is unnecessary, though. Both Fannie Mae and Freddie Mac are profitable, adding $12.9 billion and $9.3 billion in net worth in 2022, respectively," the letter stated.

Sandarciero stressed that the rule does not address the root problem of financial illiteracy in America and instead acts as a "Band-Aid."

"[This] speaks to the root of the problem which is teaching America how to save and setting young people up for success," she explained. "[It is] up to America and the government to properly guide [young people] instead of throwing credit card ads in your face [further influencing debt]."

"Now is not the time for fee increases on homebuyers."

Another major change to the rules is a new fee on borrowers with debt-to-income ratios of 40% or higher, slated to be implemented on August 1.

"NAR opposes the fee on borrowers with higher DTIs. Such a fee can change during the financing process, making it difficult to underwrite the loans. What is more, adding a fee raises the borrower’s DTI, making them more likely to default," the letter said.

The letter penned by Parcell concluded with a warning that "now is not the time for fee increases on homebuyers."

CLICK HERE TO READ MORE ON FOX BUSINESS

FOX Business' Kristen Altus and Peter Kasperowicz contributed to this report.